flowchart LR

%% Main linear flow

Acquire --> Tidy

Tidy --> Transform

%% Circular connections between Transform, Visualize, and Model

Transform <--> Visualize

Visualize <--> Model

Model <--> Transform

%% Final connections to Communicate

%% Visualize --> Communicate

Model --> Communicate

%% Styling for clean appearance

classDef default fill:#ffffff,stroke:#000000,stroke-width:2px,color:#000000,font-family:Arial,font-size:14px

class Acquire,Tidy,Transform,Visualize,Model,Communicate default

Data Science Pipeline

MScAS 2025 - DSAS Lecture 5

2025-10-21

EDA Steps

Overview

1,338 clients × 7 variables | No missing values | Ready to analyze!

Key findings

Age 18-64 | BMI mean=30.7 (overweight) | Charges: very significant range $1K-$64K!

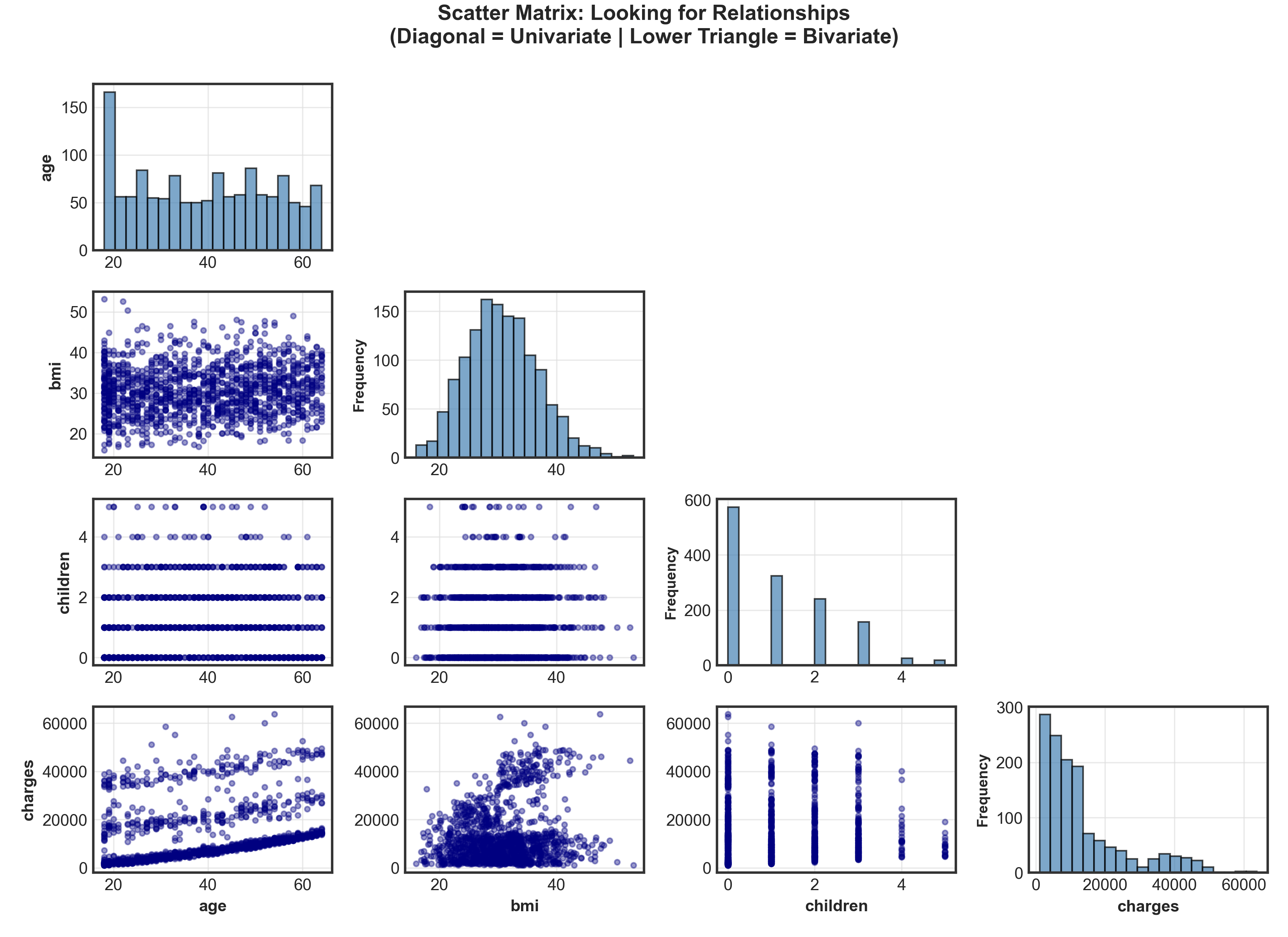

Show code

# Load data for visualization

data = pd.read_csv('healthinsurance.csv')

# Create scatter matrix with custom layout

variables = ['age', 'bmi', 'children', 'charges']

n_vars = len(variables)

fig, axes = plt.subplots(n_vars, n_vars, figsize=(11, 8))

for i in range(n_vars):

for j in range(n_vars):

ax = axes[i, j]

if i == j: # Diagonal: univariate distributions

ax.hist(data[variables[i]], bins=20, alpha=0.7, color='steelblue', edgecolor='black')

ax.set_ylabel('Frequency', fontsize=9, fontweight='bold')

elif i > j: # Lower triangle: bivariate scatter plots

ax.scatter(data[variables[j]], data[variables[i]], alpha=0.4, s=10, color='navy')

ax.set_xlabel(variables[j] if i == n_vars-1 else '', fontsize=9)

ax.set_ylabel(variables[i] if j == 0 else '', fontsize=9)

else: # Upper triangle: hide

ax.axis('off')

# Add labels to leftmost column and bottom row

for i in range(n_vars):

axes[i, 0].set_ylabel(variables[i], fontsize=10, fontweight='bold')

axes[n_vars-1, i].set_xlabel(variables[i], fontsize=10, fontweight='bold')

plt.suptitle("Scatter Matrix: Looking for Relationships\n(Diagonal = Univariate | Lower Triangle = Bivariate)",

fontsize=13, fontweight='bold', y=0.995)

plt.tight_layout()

plt.show()

Warning

Suspicious pattern spotted! Age vs. Charges shows 3 distinct groups → not random scatter!

Diving Deeper: Risk Factors

Show code

fig, axes = plt.subplots(1, 2, figsize=(10, 4.5))

# Histogram of age

_ = axes[0].hist(data['age'], bins=47, edgecolor='black', alpha=0.75, color='steelblue')

_ = axes[0].set_title("Age Distribution", fontsize=12, fontweight='bold')

_ = axes[0].set_xlabel("Age (years)", fontsize=10)

_ = axes[0].set_ylabel("Frequency", fontsize=10)

_ = axes[0].grid(True, alpha=0.3, axis='y')

# Scatter plot: Age vs Charges

_ = axes[1].scatter(data['age'], data['charges'], alpha=0.5, s=30, color='coral', edgecolors='black', linewidth=0.3)

_ = axes[1].set_title("Age vs. Annual Charges", fontsize=12, fontweight='bold')

_ = axes[1].set_xlabel("Age (years)", fontsize=10)

_ = axes[1].set_ylabel("Charges ($)", fontsize=10)

_ = axes[1].grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

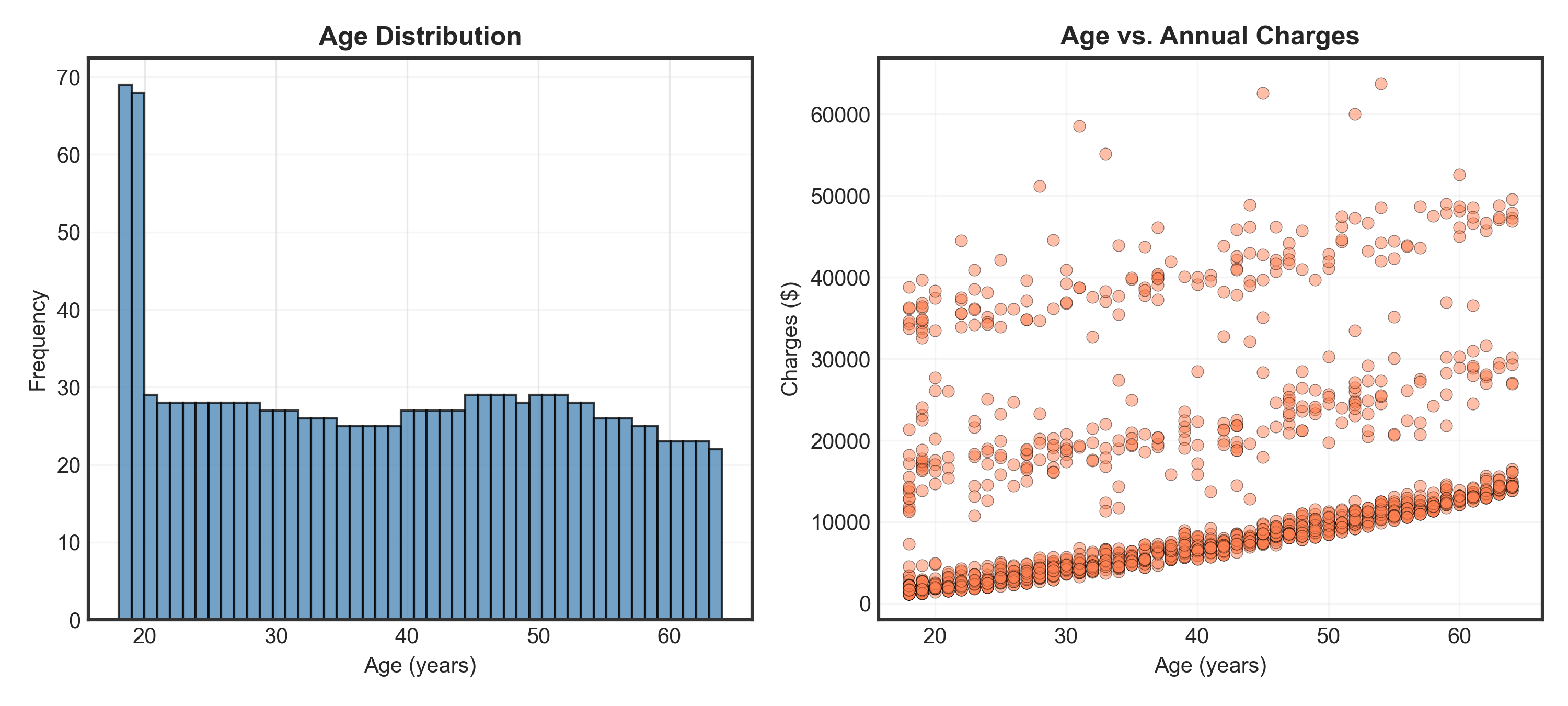

Observations

- Age: Nearly uniform distribution (except spike at 18-19 years)

- Charges: Clear 3-tier structure → low, medium, and high-cost groups! What explains this?

Show code

# Calculate percentages

smoker_counts = data.groupby('smoker').size()

total = len(data)

pct_smoker = (smoker_counts['yes'] / total) * 100

pct_nonsmoker = (smoker_counts['no'] / total) * 100

# Create scatter plot

fig, ax = plt.subplots(figsize=(10, 4.5))

colors = {'yes': 'orange', 'no': 'purple'}

for smoker_status in ['yes', 'no']:

mask = data['smoker'] == smoker_status

label = f"Smoker ({pct_smoker:.1f}%)" if smoker_status == 'yes' else f"Non-smoker ({pct_nonsmoker:.1f}%)"

_ = ax.scatter(data.loc[mask, 'age'],

data.loc[mask, 'charges'],

c=colors[smoker_status],

label=label,

alpha=0.6, s=35, edgecolors='black', linewidth=0.3)

_ = ax.set_title("Age vs. Charges (by Smoking Status)", fontsize=13, fontweight='bold')

_ = ax.set_xlabel("Age (years)", fontsize=11)

_ = ax.set_ylabel("Charges ($)", fontsize=11)

_ = ax.legend(fontsize=10, loc='upper left')

_ = ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

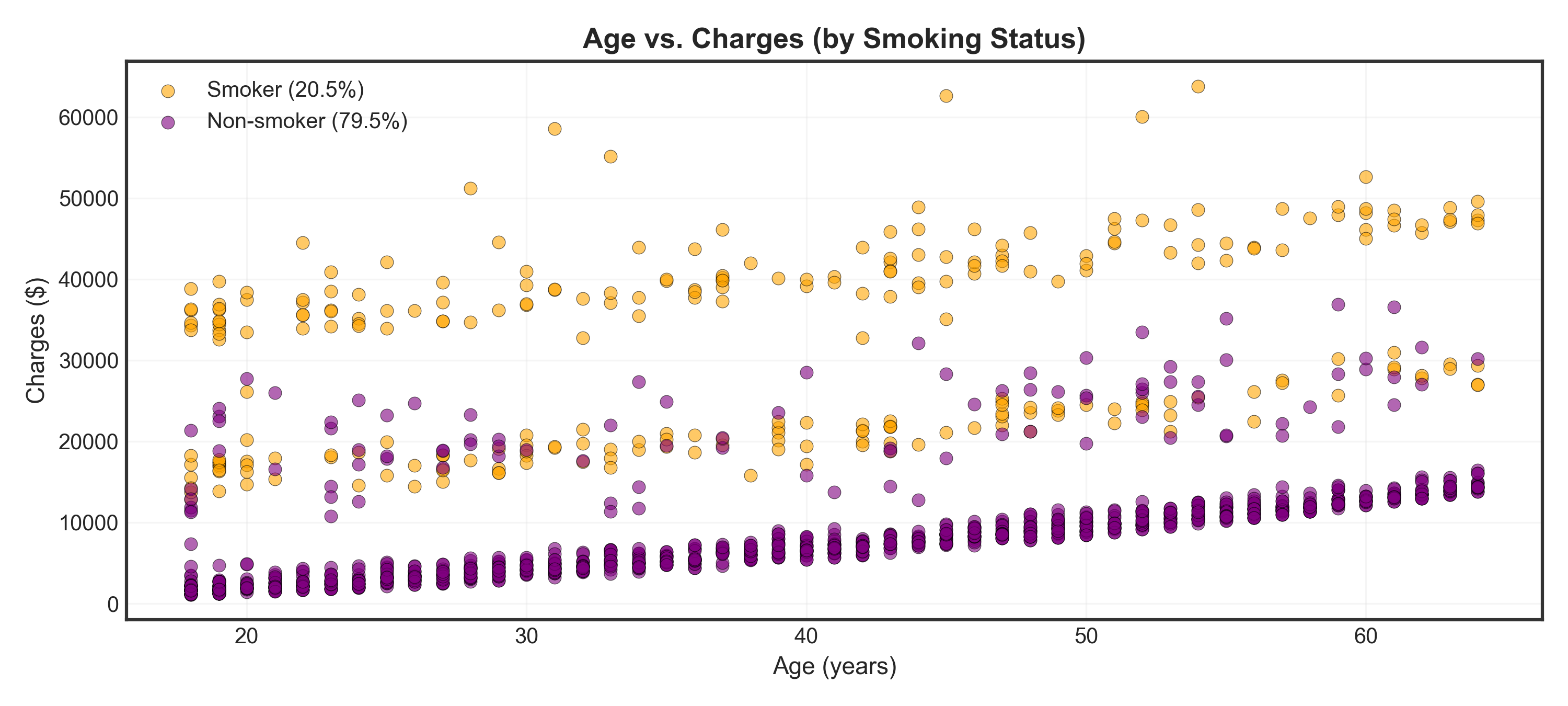

Warning

Major finding: Smokers (orange) have dramatically higher charges than non-smokers (purple) across all ages!

Show code

# --- Setup Labels ---

# 1. Define short labels for the data column and dictionary keys

short_labels = ['Underweight', 'Healthy', 'Overweight', 'Obesity', 'Severe Obesity']

# 2. Define the long, descriptive labels you want in the legend

long_labels = ['Underweight: BMI < 18.5',

'Healthy: 18.5 ≤ BMI < 25',

'Overweight: 25 ≤ BMI < 30',

'Obesity: 30 ≤ BMI < 40',

'Severe Obesity: BMI ≥ 40']

# 3. Create a "map" to link them

label_map = dict(zip(short_labels, long_labels))

# 4. Define your colors using the SHORT labels

colors_bmi = {'Underweight': 'lightblue',

'Healthy': 'green',

'Overweight': 'yellow',

'Obesity': 'orange',

'Severe Obesity': 'red'}

# --- Create BMI categories ---

# Use the SHORT labels to create the data column

data['NHS_BMI'] = pd.cut(data['bmi'],

bins=[0, 18.5, 25, 30, 40, 100],

labels=short_labels)

# --- Visualization ---

fig, ax = plt.subplots(figsize=(10, 4.5))

# Loop through the SHORT labels in REVERSE order (highest to lowest BMI)

for bmi_cat in reversed(short_labels):

mask = data['NHS_BMI'] == bmi_cat

# Skip if this category has no data (prevents errors)

if not mask.any():

continue

_ = ax.scatter(data.loc[mask, 'age'],

data.loc[mask, 'charges'],

c=colors_bmi[bmi_cat], # Uses the short label (e.g., 'Overweight')

label=label_map[bmi_cat], # Uses the map to get the long label (e.g., 'Overweight: 25 ≤ BMI < 30')

alpha=0.6, s=30, edgecolors='black', linewidth=0.3)

_ = ax.set_title("Age vs. Charges (by BMI Category)", fontsize=13, fontweight='bold')

_ = ax.set_xlabel("Age (years)", fontsize=11)

_ = ax.set_ylabel("Charges ($)", fontsize=11)

_ = ax.legend(fontsize=9, loc='upper left')

_ = ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

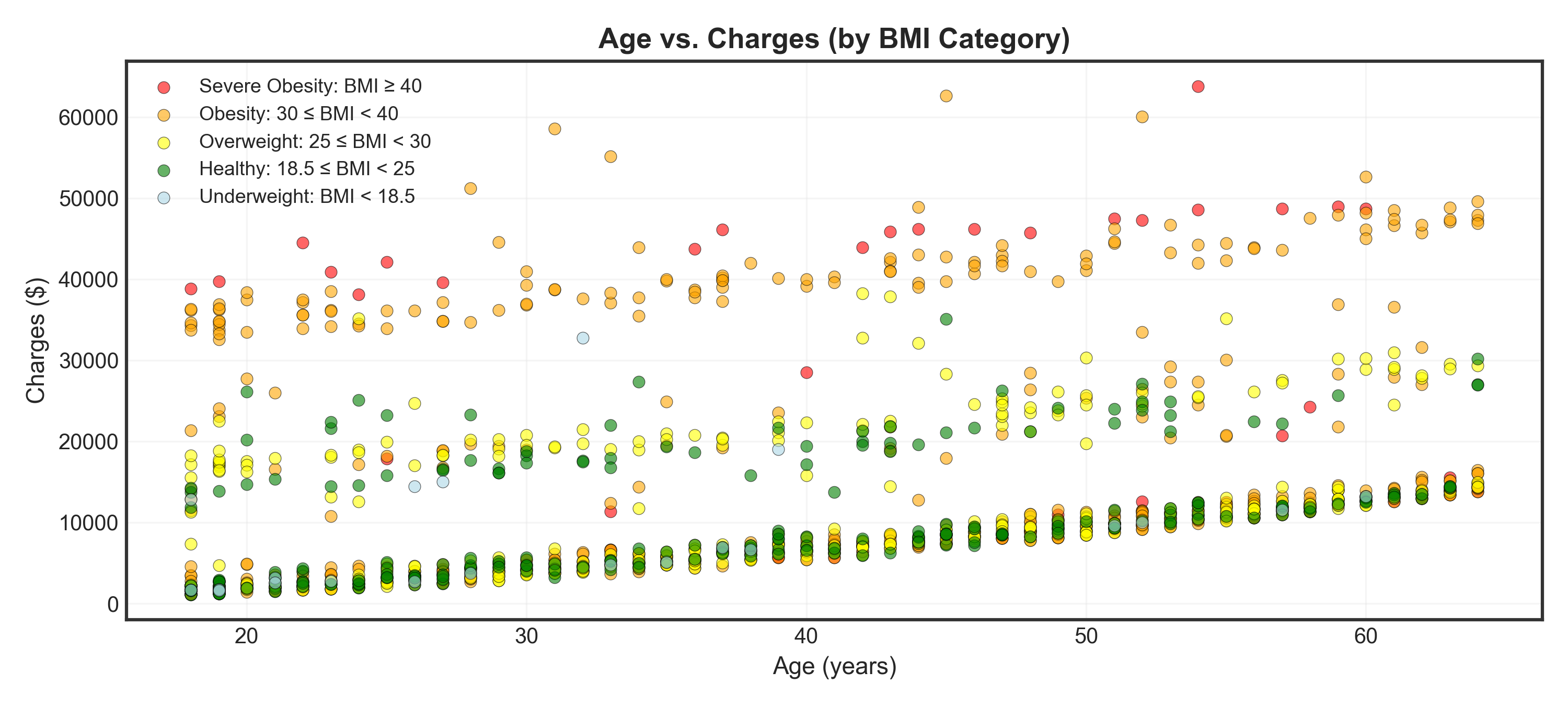

Tip

Insight: Higher BMI categories (especially severe obesity) cluster in the high-charge regions

Show code

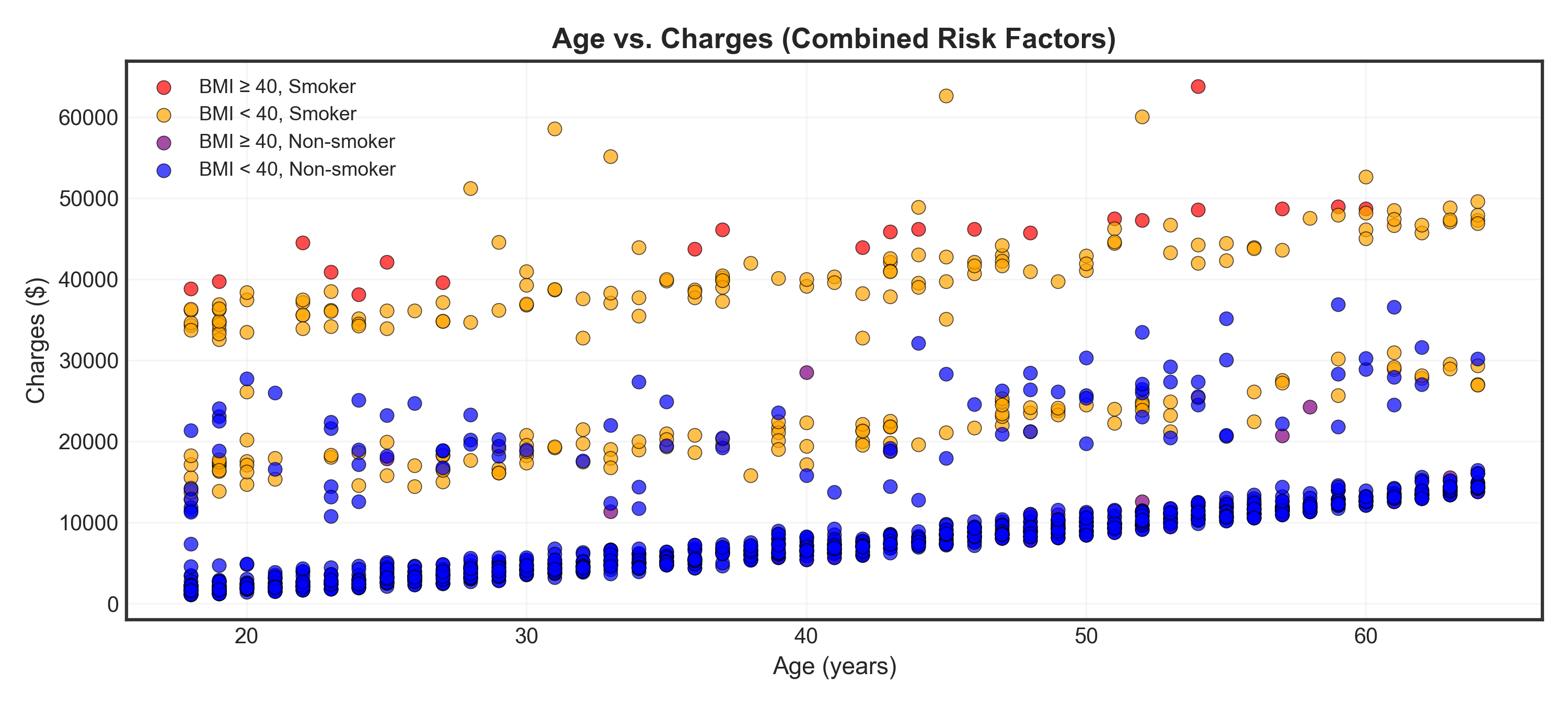

# Create combined category

data['BMI_Smoker'] = 'BMI < 40, Non-smoker'

data.loc[(data['bmi'] >= 40) & (data['smoker'] == 'no'), 'BMI_Smoker'] = 'BMI ≥ 40, Non-smoker'

data.loc[(data['bmi'] < 40) & (data['smoker'] == 'yes'), 'BMI_Smoker'] = 'BMI < 40, Smoker'

data.loc[(data['bmi'] >= 40) & (data['smoker'] == 'yes'), 'BMI_Smoker'] = 'BMI ≥ 40, Smoker'

# Visualization

fig, ax = plt.subplots(figsize=(10, 4.5))

# Define colors and order from highest to lowest risk

colors_combined = {

'BMI ≥ 40, Smoker': 'red',

'BMI < 40, Smoker': 'orange',

'BMI ≥ 40, Non-smoker': 'purple',

'BMI < 40, Non-smoker': 'blue'

}

for category in colors_combined.keys():

mask = data['BMI_Smoker'] == category

_ = ax.scatter(data.loc[mask, 'age'],

data.loc[mask, 'charges'],

c=colors_combined[category],

label=category,

alpha=0.7, s=40, edgecolors='black', linewidth=0.4)

_ = ax.set_title("Age vs. Charges (Combined Risk Factors)", fontsize=13, fontweight='bold')

_ = ax.set_xlabel("Age (years)", fontsize=11)

_ = ax.set_ylabel("Charges ($)", fontsize=11)

_ = ax.legend(fontsize=9, loc='upper left', framealpha=0.9)

_ = ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

Warning

Critical finding: High BMI (≥40) + Smoking (red points) = highest charges regardless of age!

Case Study II: Interest Rate Analysis

Swiss National Bank Yield Data

Scenario: Analyzing Swiss government bond yields for risk management.

Dataset shape: 329 observations × 14 variables

| date | 1M | 2M | 3M | 6M | 1J | 2J | 3J | 4J | 5J | 6J | 7J | 8J | 9J |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1997-12 | 1.658 | 1.883 | 2.136 | 2.384 | 2.614 | 2.821 | 3.006 | 3.171 | 3.316 | 3.445 | 3.903 | 4.167 | 4.445 |

| 1998-01 | 1.407 | 1.583 | 1.809 | 2.039 | 2.256 | 2.455 | 2.636 | 2.801 | 2.949 | 3.084 | 3.593 | 3.917 | 4.284 |

| 1998-02 | 1.128 | 1.369 | 1.619 | 1.860 | 2.084 | 2.291 | 2.481 | 2.656 | 2.816 | 2.964 | 3.543 | 3.936 | 4.408 |

| 1998-03 | 1.568 | 1.758 | 1.946 | 2.131 | 2.313 | 2.488 | 2.657 | 2.817 | 2.968 | 3.109 | 3.680 | 4.065 | 4.510 |

| 1998-04 | 1.715 | 1.981 | 2.205 | 2.403 | 2.585 | 2.756 | 2.916 | 3.068 | 3.211 | 3.344 | 3.888 | 4.255 | 4.677 |

| 1998-05 | 1.720 | 1.921 | 2.111 | 2.291 | 2.461 | 2.622 | 2.773 | 2.916 | 3.051 | 3.179 | 3.722 | 4.137 | 4.712 |

| 1998-06 | 2.117 | 2.216 | 2.333 | 2.466 | 2.608 | 2.754 | 2.899 | 3.041 | 3.178 | 3.308 | 3.851 | 4.228 | 4.674 |

| 1998-07 | 1.982 | 2.067 | 2.198 | 2.347 | 2.499 | 2.649 | 2.794 | 2.932 | 3.064 | 3.190 | 3.722 | 4.120 | 4.641 |

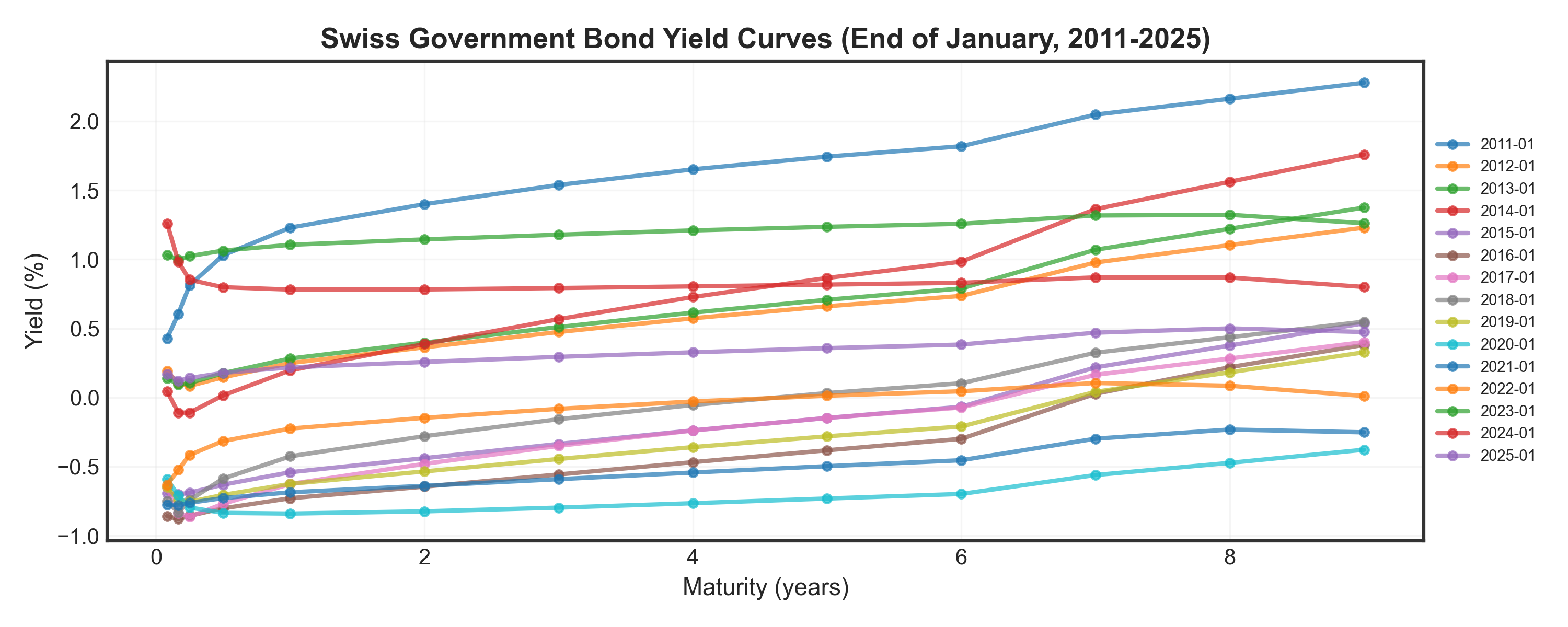

Column naming

J = Jahre (years), M = Monate (months) so 1J = 1-year, 2J = 2-year and 1M = 1-month, 6M = 6-month

Show code

# Plot yield curves over time

fig, ax = plt.subplots(figsize=(10, 4))

months = [str(i) + "-01" for i in range(2011, 2026)] # Every year, January

for month in months:

if month in df['date'].values:

yields = df.loc[df['date'] == month, df.columns[1:]].values.flatten()

_ = ax.plot(maturities, yields, marker='o', linewidth=2, markersize=4, alpha=0.7, label=month)

_ = ax.set_title("Swiss Government Bond Yield Curves (End of January, 2011-2025)", fontsize=13, fontweight='bold')

_ = ax.set_xlabel("Maturity (years)", fontsize=11)

_ = ax.set_ylabel("Yield (%)", fontsize=11)

_ = ax.legend(fontsize=7, loc='center left', bbox_to_anchor=(1, 0.5))

_ = ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

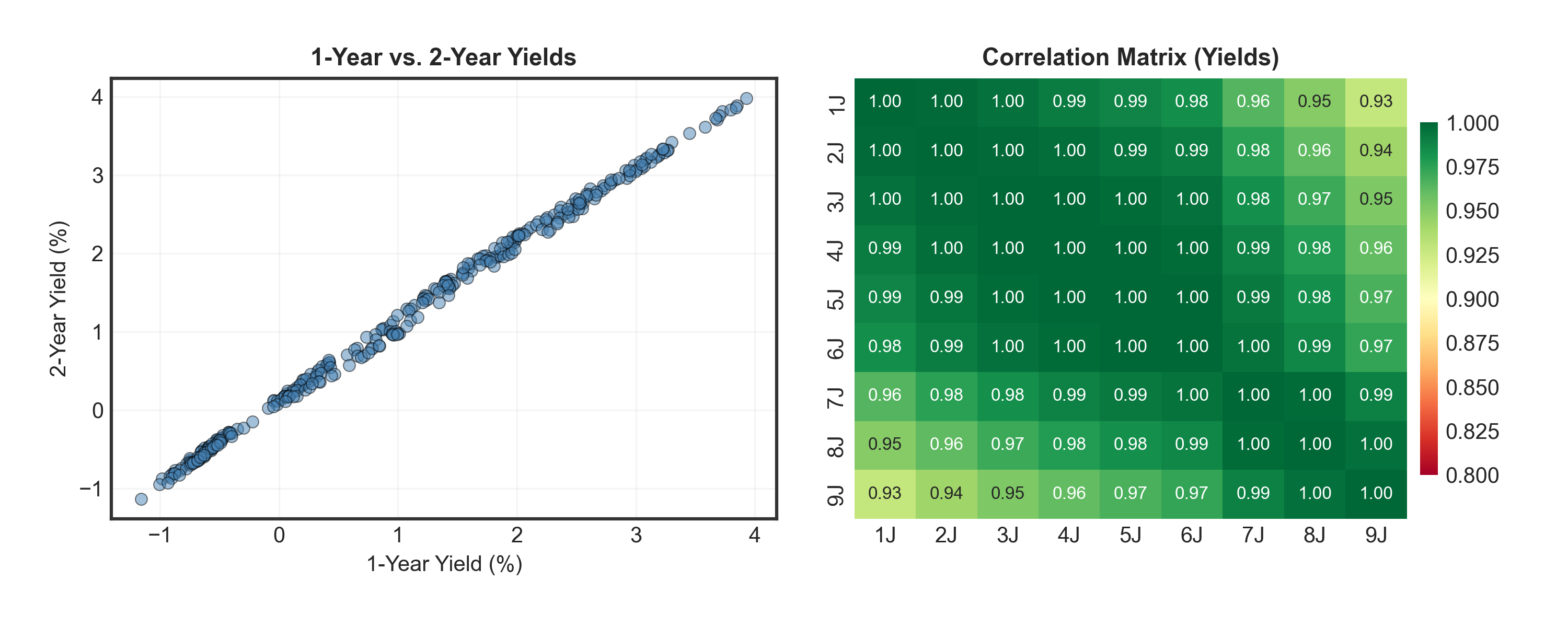

The Correlation Problem

Show code

fig, axes = plt.subplots(1, 2, figsize=(10, 4))

# Scatter plot: 1Y vs 2Y yields

_ = axes[0].scatter(df['1J'], df['2J'], alpha=0.5, s=30, color='steelblue', edgecolors='black', linewidth=0.5)

_ = axes[0].set_title("1-Year vs. 2-Year Yields", fontsize=11, fontweight='bold')

_ = axes[0].set_xlabel("1-Year Yield (%)", fontsize=10)

_ = axes[0].set_ylabel("2-Year Yield (%)", fontsize=10)

_ = axes[0].grid(True, alpha=0.3)

# Correlation heatmap

corr = df.iloc[:, 5:].corr() # Use only yearly maturities for clarity

_ = sns.heatmap(corr, annot=True, fmt=".2f", cmap="RdYlGn", ax=axes[1],

cbar_kws={'shrink': 0.8, 'pad': 0.02}, vmin=0.8, vmax=1,

annot_kws={'size': 8})

_ = axes[1].set_title("Correlation Matrix (Yields)", fontsize=11, fontweight='bold')

plt.tight_layout(pad=2.0)

plt.show()

Warning

Problem: All yields are highly correlated (0.90-0.99)! We have redundant information across many maturities (1M, 2M, 3M, 6M, 1Y, 2Y, …, 9Y).

Solution: Use Principal Component Analysis (PCA) to find the key patterns and reduce to just a few key variables!

PCA: Steps

Step 1: Normalize Data

- Convert all variables to same scale (mean=0, std=1)

- Formula: \(z_{ij} = \frac{x_{ij} - \mu_j}{\sigma_j}\)

Step 2: Compute Principal Components

- Calculate covariance matrix: \(\mathbf{\Sigma} = \frac{1}{n-1}\mathbf{X}^T\mathbf{X}\)

- Find eigenvectors & eigenvalues: \(\mathbf{\Sigma} \mathbf{v}_k = \lambda_k \mathbf{v}_k\)

- \(\mathbf{v}_k\) are eigenvectors representing the directions of principal components (the “weights”)

- \(\lambda_k\) are eigenvalues, showing the variance explained by each component

- Sort by eigenvalues (largest = most variance explained)

Step 3: Interpret Components

- PC1 (largest \(\lambda_1\) ): Captures most variance → “Level”

- PC2 (second \(\lambda_2\) ): Next most variance → “Slope” etc.

Step 4: Transform & Reconstruct

- Project data: \(\mathbf{Z} = \mathbf{X} \cdot \mathbf{V}\) (PC scores)

- Reconstruct: \(\hat{\mathbf{X}} = \mathbf{Z}_K \cdot \mathbf{V}_K^T\) (using top K components)

Key Insights

- Total variance: First few components (K=2-3) typically capture 95-99% of total variance!

- Implementation: In practice, we can use

sklearn.decomposition.PCAfrom scikit-learn.

Why Normalize?

Variables with different scales would dominate PCA. Standardization ensures equal contribution, giving each variable mean = 0 and std = 1.

Finding Principal Components

Compute the covariance matrix, find its eigenvectors (PC directions) and eigenvalues (variance explained), then sort by importance.

Tip

Key insight: First 3 components explain >99% of variation! We can safely ignore the rest.

Understanding “Weights”

The weights (eigenvector values) tell us how much each maturity contributes when a principal component changes:

- Each yield curve = weighted combination of PC1 + PC2 + PC3

- Weights = the multipliers for each maturity when that component is “activated”

- Example: If PC1 = 2.0 and 1Y weight = 0.33, then PC1 contributes 2.0 × 0.33 = 0.66% to the 1Y yield

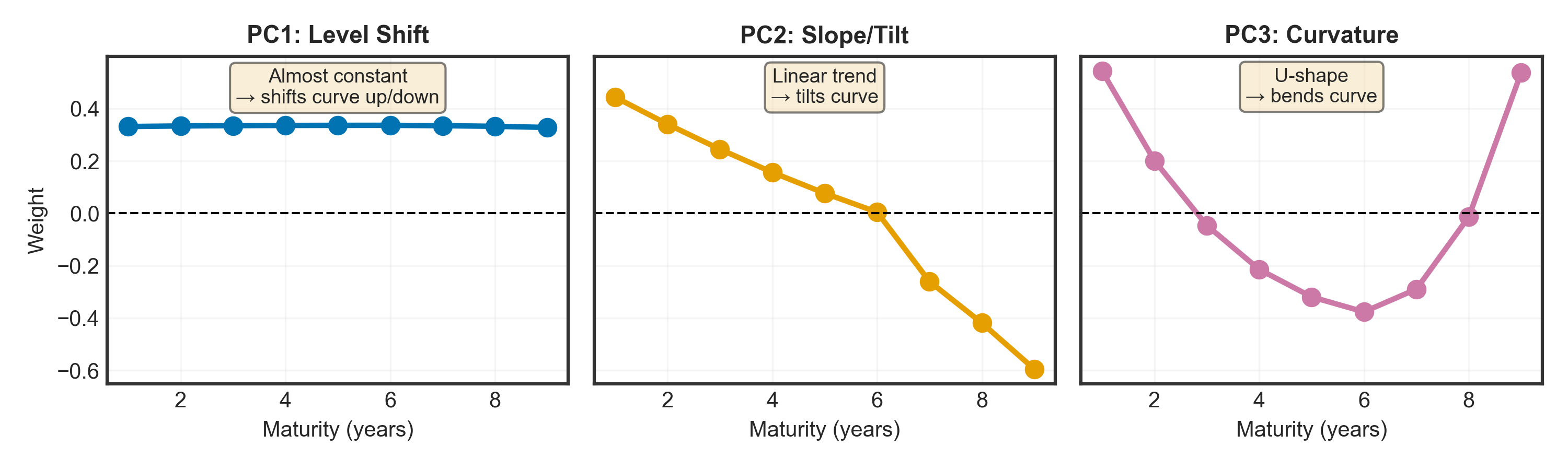

Show code

# Prepare data

df_yields = df.iloc[:, 5:] # Use only yearly maturities

mean = df_yields.mean()

std = df_yields.std()

df_norm = (df_yields - mean) / std

# Compute PCA

cov_matrix = df_norm.cov()

eigen_values, eigen_vectors = np.linalg.eig(cov_matrix)

sorted_idx = np.argsort(eigen_values)[::-1]

eigen_vectors = eigen_vectors[:, sorted_idx]

# Get first 3 PCs - make maturities list dynamic based on actual data

maturities = list(range(1, len(df_yields.columns) + 1))

pc1 = eigen_vectors[:, 0]

pc2 = eigen_vectors[:, 1]

pc3 = eigen_vectors[:, 2]

# Print actual weights for PC1 to show they're approximately equal

print("PC1 weights (1Y-9Y):", np.round(pc1, 3))

print("Theoretical equal weight for 9 variables:", np.round(1/np.sqrt(9), 3))

print("\nVerification - Each PC is normalized to length 1:")

print(f"PC1 norm: {np.linalg.norm(pc1):.6f}")

print(f"PC2 norm: {np.linalg.norm(pc2):.6f}")

print(f"PC3 norm: {np.linalg.norm(pc3):.6f}")

print("\nCross-PC sum for 1Y maturity (NOT constrained to 1):")

print(f"PC1[1Y] + PC2[1Y] + PC3[1Y] = {pc1[0]:.3f} + {pc2[0]:.3f} + {pc3[0]:.3f} = {pc1[0] + pc2[0] + pc3[0]:.3f}")

# Example reconstruction for first observation

print("\nExample: Reconstructing 1Y yield for first date:")

pc_scores = df_norm.dot(eigen_vectors)

first_date_1y_norm = pc_scores.iloc[0, 0] * pc1[0] + pc_scores.iloc[0, 1] * pc2[0] + pc_scores.iloc[0, 2] * pc3[0]

first_date_1y_actual = df_norm.iloc[0, 0]

print(f" PC1_score × PC1_weight[1Y] + PC2_score × PC2_weight[1Y] + PC3_score × PC3_weight[1Y]")

print(f" = {pc_scores.iloc[0, 0]:.3f} × {pc1[0]:.3f} + {pc_scores.iloc[0, 1]:.3f} × {pc2[0]:.3f} + {pc_scores.iloc[0, 2]:.3f} × {pc3[0]:.3f}")

print(f" = {first_date_1y_norm:.3f}")

print(f" Actual normalized 1Y yield: {first_date_1y_actual:.3f}")

print(f" Match: {np.isclose(first_date_1y_norm, first_date_1y_actual)}")

# Plot

fig, axes = plt.subplots(1, 3, figsize=(10, 3), sharey=True)

_ = axes[0].plot(maturities, pc1, marker='o', linewidth=2.5, markersize=8, color='#0173B2')

_ = axes[0].axhline(y=0, color='black', linestyle='--', linewidth=1)

_ = axes[0].set_title("PC1: Level Shift", fontsize=11, fontweight='bold')

_ = axes[0].set_xlabel("Maturity (years)", fontsize=10)

_ = axes[0].set_ylabel("Weight", fontsize=10)

_ = axes[0].grid(True, alpha=0.3)

_ = axes[0].text(5, max(pc1)*1.25, "Almost constant\n→ shifts curve up/down",

ha='center', fontsize=9, bbox=dict(boxstyle='round', facecolor='wheat', alpha=0.5))

_ = axes[1].plot(maturities, pc2, marker='o', linewidth=2.5, markersize=8, color='#E69F00')

_ = axes[1].axhline(y=0, color='black', linestyle='--', linewidth=1)

_ = axes[1].set_title("PC2: Slope/Tilt", fontsize=11, fontweight='bold')

_ = axes[1].set_xlabel("Maturity (years)", fontsize=10)

_ = axes[1].grid(True, alpha=0.3)

_ = axes[1].text(5, max(pc2)*0.95, "Linear trend\n→ tilts curve",

ha='center', fontsize=9, bbox=dict(boxstyle='round', facecolor='wheat', alpha=0.5))

_ = axes[2].plot(maturities, pc3, marker='o', linewidth=2.5, markersize=8, color='#CC79A7')

_ = axes[2].axhline(y=0, color='black', linestyle='--', linewidth=1)

_ = axes[2].set_title("PC3: Curvature", fontsize=11, fontweight='bold')

_ = axes[2].set_xlabel("Maturity (years)", fontsize=10)

_ = axes[2].grid(True, alpha=0.3)

_ = axes[2].text(5, max(pc3)*0.78, "U-shape\n→ bends curve",

ha='center', fontsize=9, bbox=dict(boxstyle='round', facecolor='wheat', alpha=0.5))

plt.tight_layout()

plt.show()

What Do These Components Actually Mean?

PC1: Level Shift (~98.44% of variance)

- Weights: All maturities ≈ 0.33 (almost equal and positive)

- Interpretation: All yields move together by the same amount

- When PC1 score increases by 1 → ALL rates shift up by ~0.33% in parallel

- Real example: Central bank raises policy rate → entire curve moves up together (inflation shock)

PC2: Slope/Tilt (~1.46% of variance)

- Weights: Short-term: positive (+0.4) | Long-term: negative (-0.6)

- Interpretation: Short and long rates move in opposite directions

- When PC2 score increases → short rates ↑ & long rates ↓ → curve flattens

- Real example: Recession fears → long rates drop (expect rate cuts), short rates stay high

PC3: Curvature (~0.09% of variance)

- Weights: Ends: positive | Middle (4-6Y): negative

- Interpretation: Middle maturities move opposite to short/long ends

- When PC3 score increases → middle bends down, ends bend up → humped curve

- Real example: Expect rates to rise then fall → medium-term rates peak

In simple terms: PC1 score = “How high is the curve?”, PC2 score = “How steep?”, PC3 score = “How curved?”

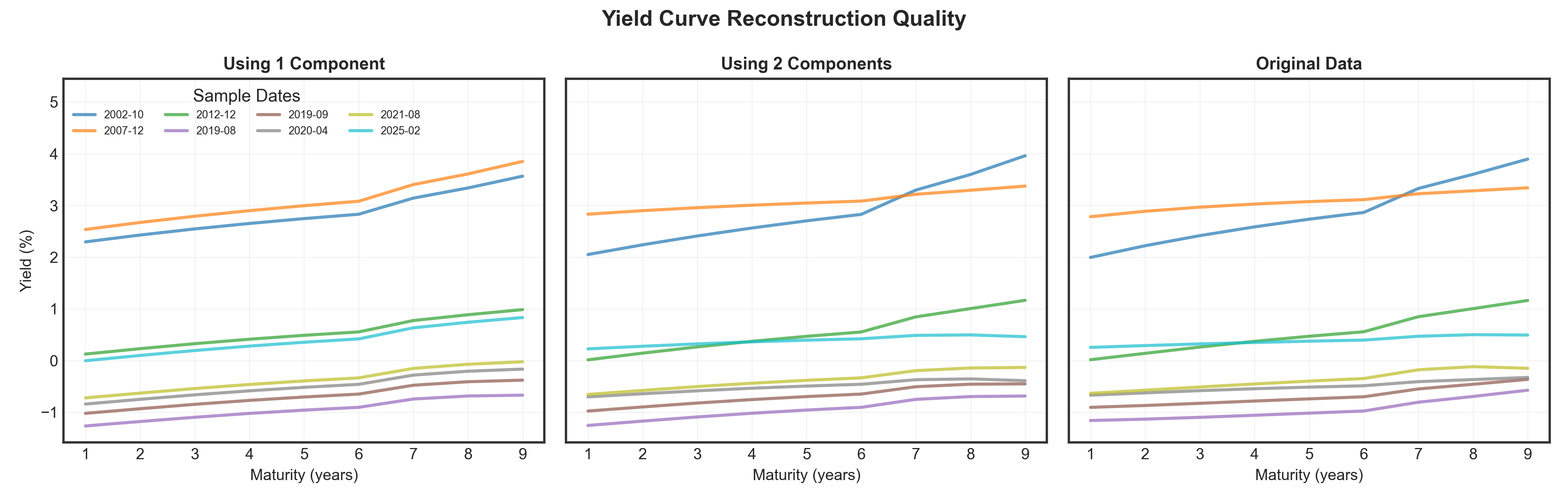

Transform & Reconstruct

Project the normalized data onto principal components, then reconstruct using only the top K components.

Show code

# Transform data to PC space

PC_scores = df_norm.dot(eigen_vectors)

# Select some random bond dates to track consistently

np.random.seed(1)

sample_indices = np.random.choice(len(df_norm), size=8, replace=False)

sample_indices = sorted(sample_indices)

# Use only the 9 yearly maturities that match our PCA dimensions

maturities = list(range(1, 10)) # 1Y through 9Y to match the 9 columns we used for PCA

# Create 3 panels: 1 Component, 2 Components, Original

fig, axes = plt.subplots(1, 3, figsize=(14, 4.5), sharey=True)

colors = plt.cm.tab10(np.linspace(0, 1, len(sample_indices)))

# Store all data for consistent y-axis scaling

all_data = []

# Panel 1: Reconstruction with 1 component

reconstructed_1 = PC_scores.iloc[:, :1].dot(eigen_vectors[:, :1].T)

reconstructed_1_denorm = reconstructed_1 * std.values + mean.values

all_data.extend(reconstructed_1_denorm.values.flatten())

for idx, sample_idx in enumerate(sample_indices):

date_label = df['date'].iloc[sample_idx]

axes[0].plot(maturities, reconstructed_1_denorm.iloc[sample_idx],

alpha=0.7, linewidth=2, color=colors[idx], label=date_label)

axes[0].set_title("Using 1 Component", fontsize=11, fontweight='bold')

axes[0].set_xlabel("Maturity (years)", fontsize=10)

axes[0].set_ylabel("Yield (%)", fontsize=10)

axes[0].grid(True, alpha=0.3)

# Panel 2: Reconstruction with 2 components

reconstructed_2 = PC_scores.iloc[:, :2].dot(eigen_vectors[:, :2].T)

reconstructed_2_denorm = reconstructed_2 * std.values + mean.values

all_data.extend(reconstructed_2_denorm.values.flatten())

for idx, sample_idx in enumerate(sample_indices):

axes[1].plot(maturities, reconstructed_2_denorm.iloc[sample_idx],

alpha=0.7, linewidth=2, color=colors[idx])

axes[1].set_title("Using 2 Components", fontsize=11, fontweight='bold')

axes[1].set_xlabel("Maturity (years)", fontsize=10)

axes[1].grid(True, alpha=0.3)

# Panel 3: Original data

for idx, sample_idx in enumerate(sample_indices):

original = df_yields.iloc[sample_idx].values

all_data.extend(original)

axes[2].plot(maturities, original,

alpha=0.7, linewidth=2, color=colors[idx])

axes[2].set_title("Original Data", fontsize=11, fontweight='bold')

axes[2].set_xlabel("Maturity (years)", fontsize=10)

axes[2].grid(True, alpha=0.3)

# Set consistent y-axis limits across all panels

y_min, y_max = min(all_data), max(all_data)

y_margin = (y_max - y_min) * 0.05

for ax in axes:

ax.set_ylim(y_min - y_margin, y_max + y_margin)

# Add overall title

fig.suptitle('Yield Curve Reconstruction Quality', fontsize=14, fontweight='bold', y=0.98)

# Add legend to the first panel only with 2 rows (horizontal layout)

axes[0].legend(title='Sample Dates', fontsize=7, loc='upper left', framealpha=0.9, ncol=4)

plt.tight_layout()

plt.show()

Result

Just 3 numbers (PC1, PC2, PC3 scores) capture nearly all information in 13 yields! Notice how 1 component is too simple (flat), 2 components add slope, and 3 components capture full curve shapes.

Case Study II: PCA Summary

Key Results

Dimensionality Reduction

- 9 correlated yields (13 in total) → 3 uncorrelated components

- 99.9% of variance retained

- Minimal information loss

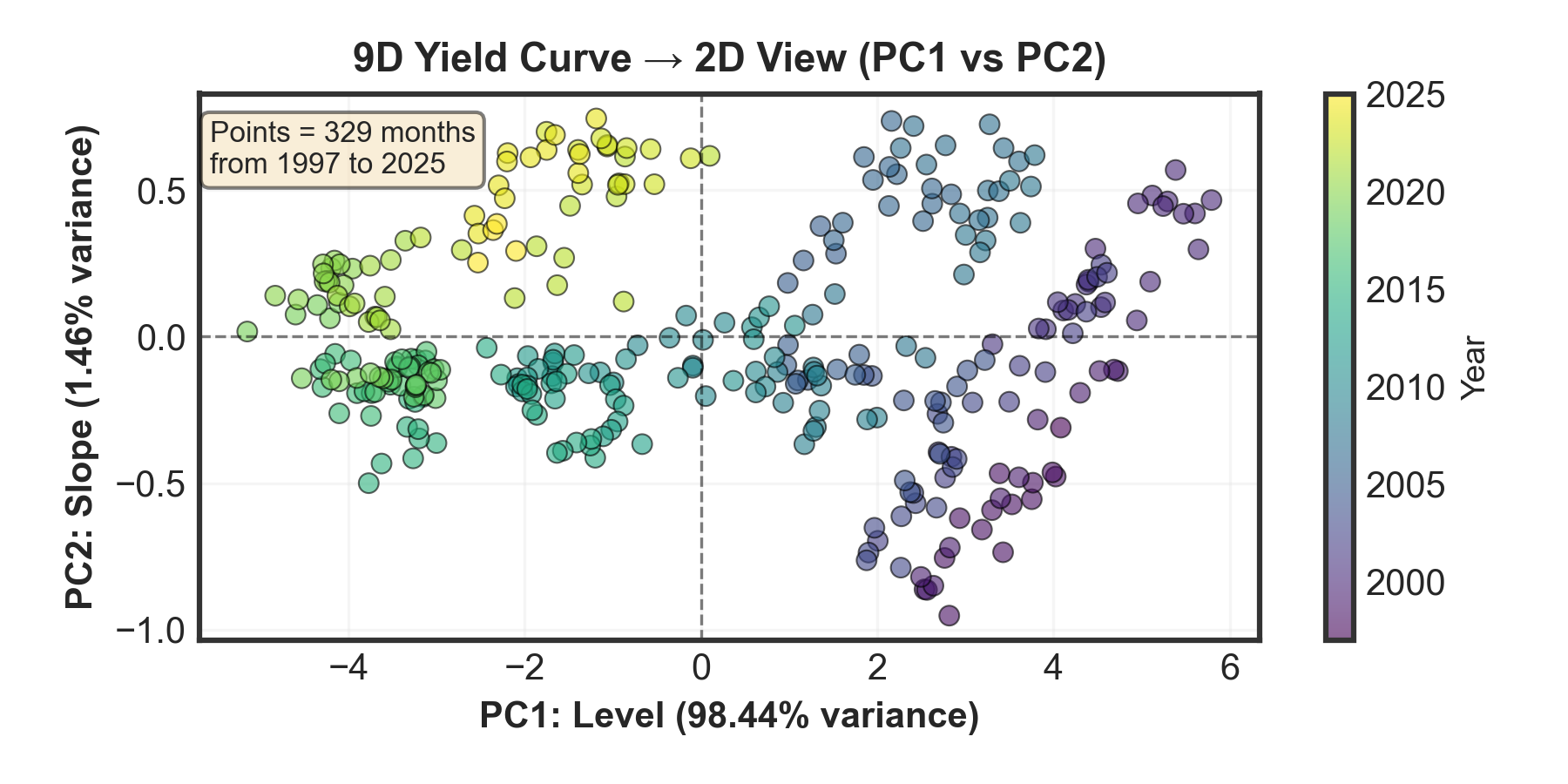

Three Components & 2D Plot Interpretation:

PC1 (Level): 98.44% variance — Parallel shift of entire curve

Horizontal axis: Movement left/right = interest rates rising/falling overallPC2 (Slope): 1.46% variance — Curve steepening/flattening

Vertical axis: Movement up/down = yield curve steepening/flatteningPC3 (Curvature): 0.09% variance — Mid-curve bending

Practical Value

When to use PCA:

- Many correlated variables

- Need dimensionality reduction

- Want to remove noise

- Linear relationships in data

Real applications:

- Interest rate modeling

- Portfolio risk analysis

- Customer segmentation

- Image compression

Important limitations:

- Only captures linear patterns

- Requires standardization

- Components are abstract

- Sensitive to outliers